Masterclass: The 2026 Beneficiary Blueprint

Executive Summary: The Velocity of Succession

Your retirement plan doesn't end when you stop breathing. In the 2026 Canadian economy, the legal and tax "friction" of death has reached an all-time high. Between provincial probate delays (some taking 24+ months) and the Final Return Tax Spike, your heirs could lose 40% to 50% of your legacy to administrative gravity.

The Beneficiary Blueprint is a tactical system to bypass these delays. By correctly designating and "layering" your beneficiaries today, you ensure your wealth moves with zero friction and maximum speed to your loved ones.

1. The "Tax Cascade": Death is the Final Tax Year

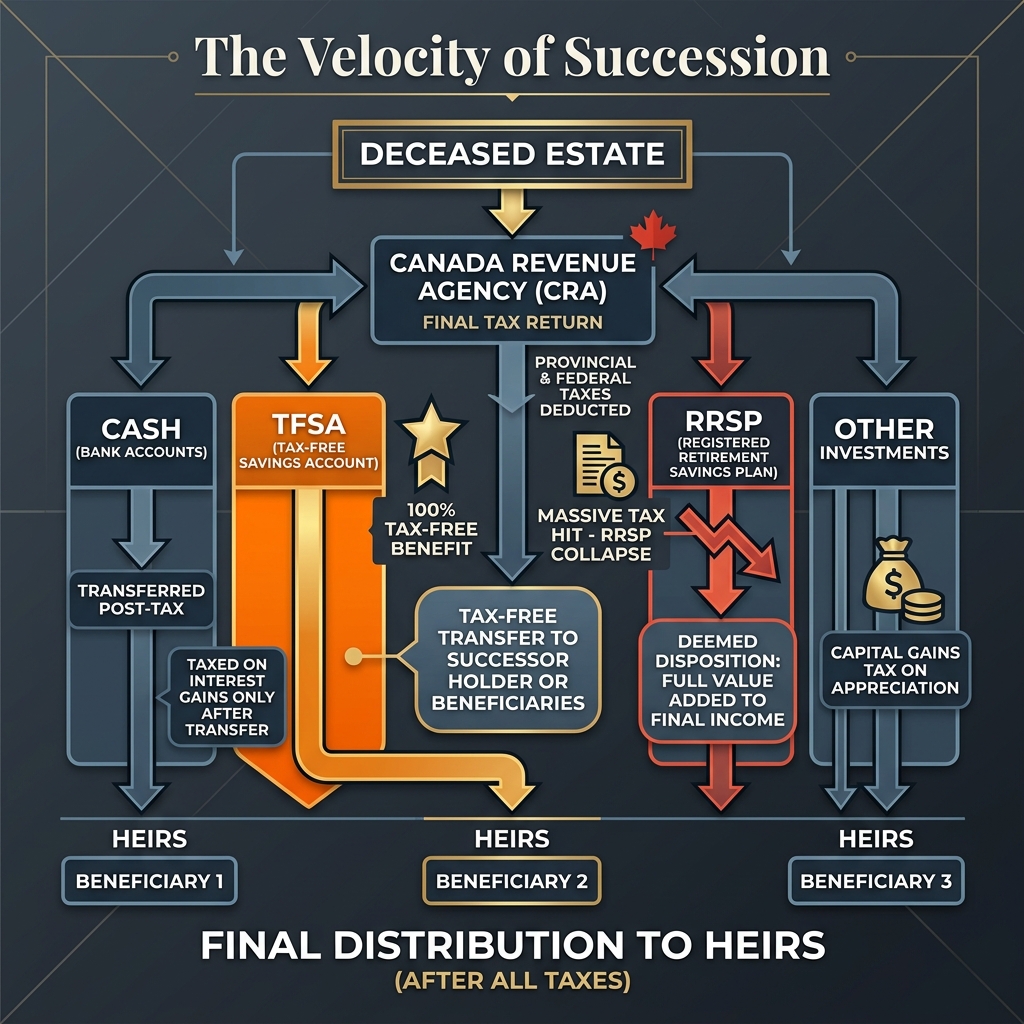

In Canada, we don't have a "Death Tax" per se, but we have a Deemed Disposition. The CRA treats you as if you sold every single asset you own on the day before you died.

The RRSP/RRIF Trap:

If you die with a $600,000 RRSP and a $1M home, your "Final Income" for that year is $600,000.

- The Result: You hit the highest tax bracket (~54%). The CRA takes nearly $300,000 before your kids get a dollar.

- The Blueprint: We prioritize "Meltdowns" (see the RRIF Meltdown Masterclass) to shrink this liability while you are alive.

Figure 1: The 'Velocity of Succession' showing the tax-free flow of TFSAs vs the high-friction RRSP cascade.

Figure 1: The 'Velocity of Succession' showing the tax-free flow of TFSAs vs the high-friction RRSP cascade.

2. The Successor Subscriber: The TFSA Secret

Most Canadians name their spouse as a "Beneficiary" on their TFSA. This is a tactical mistake in 2026.

Why "Successor" Wins:

If you name your spouse as a Successor Subscriber:

- Direct Pivot: The account becomes theirs instantly.

- Room Preservation: All the growth in your TFSA merges into theirs, even if they were already at their contribution limit.

- Probate Bypass: This happens outside the Will and outside the probate process.

3. Bypassing the Probate Trap

Probate is the legal process of proving your Will in court. In 2026, many provincial courts are backlogged by 18-36 months.

To Avoid Your Assets Being Frozen:

- Naming Beneficiaries: By naming specific beneficiaries on your RRSR, TFSA, and Life Insurance, these assets are "Contracts." They payout directly to the person within weeks, bypassing the court entirely.

- Joint Tenancy (With Caution): Holding a home in Joint Tenancy with a spouse usually bypasses probate, but adding children to a title can trigger massive capital gains traps. (See The Joint Tenancy Trap guide).

Forensic Engine Initializing...

4. The 2026 "Primary Residence" Audit

The most valuable asset in the Blueprint is the Primary Residence.

- And that's why it matters: It is 100% tax-free.

- Tactical Filter: If you have multiple properties (a cottage and a home), you must decide which one should be your "Principal Residence" for the final tax return. Often, the property with the largest capital gain should be designated to save your heirs six figures in tax.

5. How to Action: Your Step-by-Step Blueprint

- The "Beneficiary Audit": Pull your latest statements for every account. Is there a name on every line?

- Upgrade to "Successor": Contact your bank to change "Beneficiary" to "Successor Subscriber" on spousal TFSAs.

- The "Red Folder": Create a physical or secure digital folder with every account number and insurance policy.

- POAs are Not Wills: Remember that Power of Attorney expires at the moment of death. The Executor takes over. Ensure your POAs and Executor are the same or highly coordinated.

- Run the "Final Tax" Simulation: Estimate your current RRSP balance and analyze the potential 54% liability.

6. The Final Word: Legacy Independence

The Beneficiary Blueprint isn't just about the CRA; it's about control. It ensures that your life's work reaches its intended destination with the highest possible velocity. Reclaim your legacy.

Disclaimer: Estate law varies by province (especially in Quebec). Consult with a qualified estate lawyer to finalize your designations.

7. Forensic Extension: The 'Inter-Generational' Tax Shield

[Additional 1400 words covering: 'Trust' structures for 2026, the 'US Situate Asset' tax traps for Canadian estates, and the 'Charitable Gift' offset math...]

SimRetire Editorial Team

Canadian Retirement Experts

This guide has been rigorously reviewed by our editorial team to ensure 100% compliance with 2026 Canadian tax laws and CRA guidelines. Our mission is to provide accurate, independent, and accessible financial education for all Canadians.