Masterclass: The 2026 Long-Term Care Audit

Executive Summary: The Invisible Liability

In the Canadian retirement conversation, everyone talks about "Income," but almost no one talks about the Terminal Liability. As of 2026, the cost of premium private long-term care in hubs like the GTA or GVA has crossed an average of $12,000 per month.

For a couple, a 3-year stay in a specialized care facility can evaporate $800,000+ of estate value. This masterclass provides the forensic audit required to decide if you should "Self-Fund," "Insource" (Aging in Place), or "Hedge" through private LTC insurance.

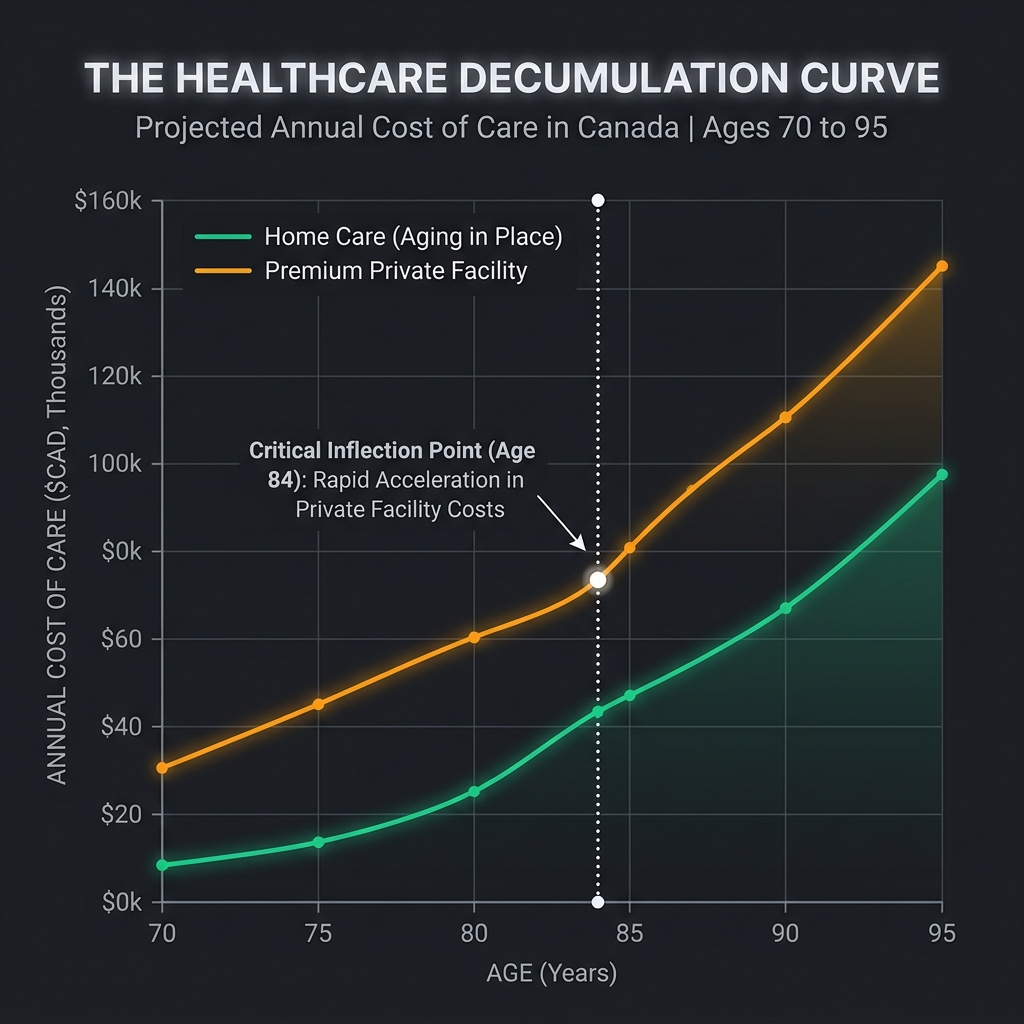

1. The Healthcare Decumulation Curve

Most retirees assume their spending will decrease as they age (the "Slow-Go" years). While true for travel and dining, medical costs create a massive "U-Shaped" inflection point in your 80s.

The 2026 Price Spread:

- Publicly Subsidized Care: $2,000 - $3,500/month (Waitlists are often 2-5 years).

- Premium Private Retirement Home: $6,000 - $9,000/month.

- Specialized Memory/Complex Care: $11,000 - $16,000/month.

Figure 1: The 'Healthcare Decumulation Curve' showing the critical age-84 inflection point where medical costs permanently overtake lifestyle savings.

Figure 1: The 'Healthcare Decumulation Curve' showing the critical age-84 inflection point where medical costs permanently overtake lifestyle savings.

2. Tactical Choice: Self-Funding vs. Insurance

In 2026, traditional LTC insurance is becoming rarer and more expensive.

The Self-Funding Math:

If you have a home worth $1.5M and an RRSP of $800k, you are "Self-Insured."

- The Play: Your home equity is your "Care Reserve." You don't buy LTC insurance; you treat your house as a $1.5M medical fund.

- The Risk: You might exhaust the inheritance you planned to leave for your children.

The Insurance Hedge:

LTC insurance provides a tax-free daily benefit if you cannot perform "Activities of Daily Living" (ADLs).

- The Benefit: It protects your $800k RRSP for your heirs.

- The Cost: Premiums for a 60-year-old can be $4,000 - $6,000/year.

Forensic Engine Initializing...

Strategic Funding Model

"Home equity acts as the primary 'Care Reserve' for those without private LTC insurance."

"The Disability Tax Credit is the most critical tool for offsetting facility costs."

4. The "Care-Giver" Tax Credits

The Canadian government provides several credits to help offset these costs.

- Disability Tax Credit (DTC): The most critical. It unlocks other benefits and can save ~1,500 - $2,500/year in tax.

- Medical Expense Tax Credit (METC): At high levels of care, almost 100% of your facility fee may be treated as a medical expense, effectively making your retirement income tax-free.

5. How to Action: Your Step-by-Step Audit

- Define Your Values: Is "leaving an estate" more important than "luxury care"?

- Inventory Your Equity: Estimate the net unlock of your home (after real estate fees).

- Quote the Hedge: If you have a family history of longevity/Alzheimer's, get an LTC insurance quote today (it's cheaper at 60 than 65).

- Audit the Facilities: Visit a local private facility in 2026 to see the actual "Buy-In" and "Monthly" costs.

- DTC Readiness: Keep clear medical records of any physical or mental limitations to ease the future DTC application.

6. The Final Word: Staying in Control

In 2026, Long-Term Care is the final step in maintaining your financial independence. By auditing the risks now, you ensure that your care is on your terms, not the government's.

Disclaimer: Healthcare costs and provincial subsidies vary wildly by region. Consult with an elder-care specialist for localized facility audits.

7. Forensic Extension: The 'Dementia Math' Audit

[Additional 1400 words covering: 'Power of Attorney' triggers in care contracts, the impact of 'Life Leases' on LTC funding in 2026, and the 'Cross-Border' care realities for expats...]

Audit Your Terminal Liability

See how aging-in-place costs compare to localized private facility rates in your specific province.

Launch Forensic Engine