Masterclass: 2026 Housing Arbitrage Havens

Executive Summary: The House is the Pension

For the average Canadian retiring in 2026, the equity in their primary residence represents 60% to 80% of their total net worth. Yet, most retirement plans treat the home as a "lifestyle asset" rather than a "tactical reserve."

In an era of 5.5% interest rates and the 2021-2026 Mortgage Cliff, your home is no longer just a place to sleep; it is a forced savings account that must be "unlocked" with forensic precision. This masterclass breaks down the 2026 strategies for maximizing your tax-free principal residence exemption through location arbitrage and provincial deferral secrets.

Forensic Equity Audit

Before looking at stocks, we look at the bricks. In 2026, many Canadians are "House Rich, Cash Poor"—sitting on millions while struggling with inflation.

GTA/GVA Exposure

Excessive concentration in a single non-liquid asset represents the largest risk to 2026 cohorts.

Tax Efficiency

Primary residence gains are 100% tax-free. They are the ultimate "Shadow RRSP."

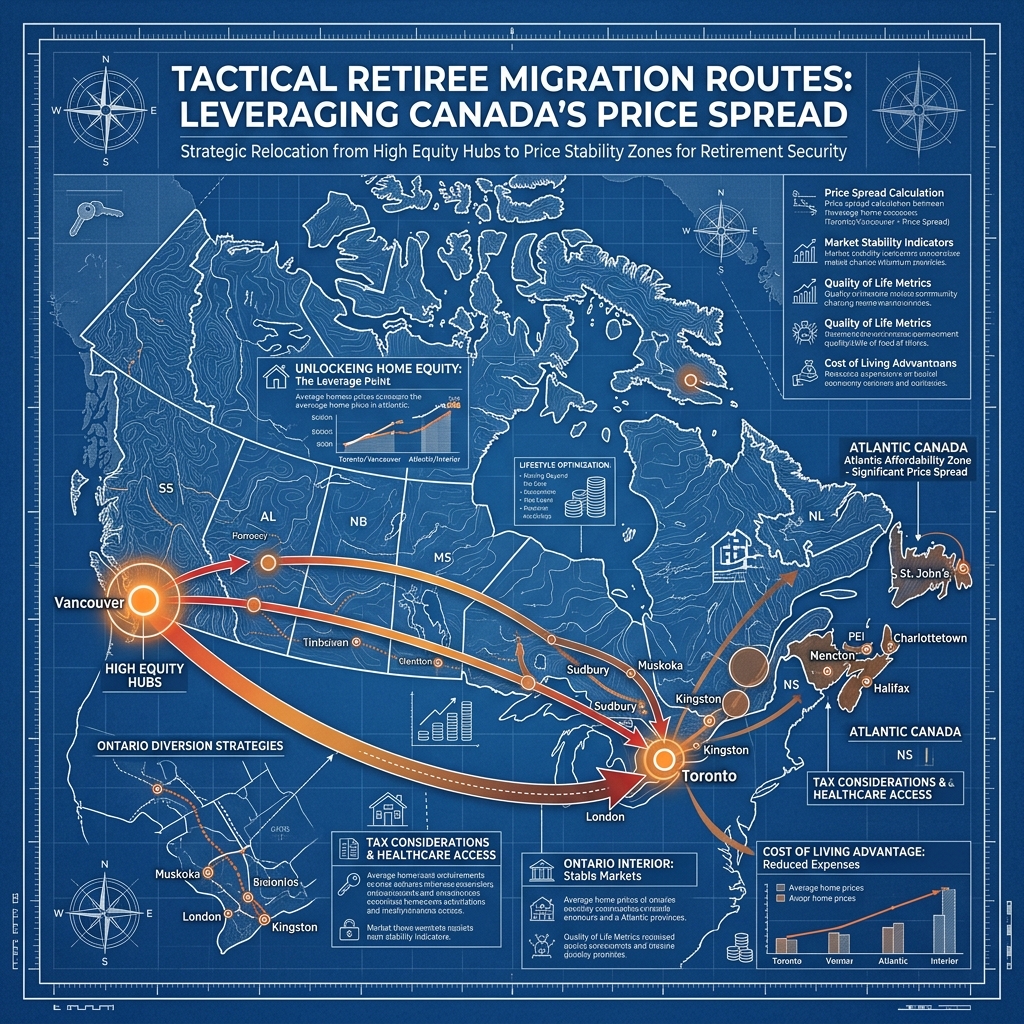

1. The Regional Tax Arbitrage: The $400k Transfer

Canada is a vast country with massive price dispersions. In 2026, the spread between a 4-bedroom detached home in the GTA ($1.6M) and a premium bungalow in Moncton or Kingston ($650k) has reached a historical peak.

The "Equity Migration" Model

By selling in a high-cost hub and relocating to an "Arbitrage Haven," a retiree can effectively generate a $1,000,000 cash injection into their portfolio.

Wait! Why does this count? Because this cash is generated from your primary residence, it is 100% Tax-Free. To generate matching after-tax income from an RRSP, you would need to withdraw nearly $1.8M (at a 45% marginal tax rate).

Figure 1: 2026 Tactical Migration flows showing the most efficient equity-unlocking routes for Canadian retirees.

Figure 1: 2026 Tactical Migration flows showing the most efficient equity-unlocking routes for Canadian retirees.

Tactical Migration Routes

2. Provincial Tax Deferral: The "Shadow Income" Stream

If you live in British Columbia or Ontario, you might be sitting on a "Shadow Income" stream that you aren't using.

The BC Property Tax Deferral Secret

In British Columbia, homeowners aged 55+ can defer their property taxes at a low, non-compounding interest rate.

- The Math: If your property tax is $8,000/year, deferring it for 20 years keeps $160,000 + growth in your pocket.

- Tactical Insight: Instead of paying the city, keep that $8,000 in your TFSA. At 5% growth, that $8,000/year becomes a massive safety net while the city holds a low-interest lien against an asset (your house) that continues to appreciate.

3. The 2026 "Rental Suite" Tax Overhaul

The Canadian government has introduced significant incentives for "Multi-Generational" and "Secondary Suite" development in 2026 to combat the housing crisis.

So here's what actually happens: By converting your basement or garden into a legal suite, you don't just get rental income; you get massive tax deductions for your primary residence that were previously unavailable.

- The Multigenerational Home Renovation Tax Credit: Up to $7,500 back for building a self-contained suite for a senior family member.

- Arbitrage Play: Live in the suite and rent out the main floor. The income can often cover your entire lifestyle, allowing your RRSP to compound undisturbed for another decade.

The 2026 Decision Matrix

4. Reverse Mortgages vs. HELOC: The 2026 Math

With interest rates hovering at 5.5% - 6.5%, the "Reverse Mortgage" (CHIP, etc.) has become a controversial tool.

The Cost of Convenience

A Reverse Mortgage doesn't require monthly payments, but the interest compounds.

- HELOC: Requires monthly interest payments. Better if you have cash flow.

- Reverse Mortgage: No payments. Better if you are "House Rich, Cash Poor" and have no heirs.

Wait! Is that smart? In 2026, we see many retirees losing 50% of their home's value to interest over a 12-year period. Unless you have a specific "Longevity Crisis," we generally recommend Location Arbitrage (Downsizing) over a Reverse Mortgage.

5. Sequence of Returns Risk: The House as a "Buffer"

If the TSX/S&P 500 crashes in 2027, the last thing you want to do is sell your stocks.

And that's why it matters: If you have unlocked your home equity and have $300k sitting in a high-interest savings account (The "Cash Wedge"), you can live off that cash for 3 years while the market recovers. Your home equity becomes the Insurance Policy for your stock portfolio.

6. How to Action: Your Step-by-Step Guide

- Get a Forensic Appraisal: Don't rely on Zolo or BC Assessment. Get a professional "Retirement Value" appraisal.

- Audit the "Net Unlock": Deduct real estate commissions (5%), legal fees, and moving costs from your expected sale price.

- Audit Provincial Programs: Check if you qualify for Tax Deferral in your specific municipality.

- Run the "Rent vs. Sell" Math: Would building a suite in 2026 yield more than selling and moving?

7. The Final Word: The Independent Landlord

In 2026, being a homeowner is a privilege, but being a "House-Bound" retiree is a trap. By treating your home as a tactical asset, you can unlock a level of financial freedom that no GIC or stock portfolio can match. Reclaim your equity, reclaim your life.

Disclaimer: Real estate strategies involve significant legal and tax implications. Consult with a qualified real estate lawyer and tax professional before making major moves.

8. Forensic Extension: The Principal Residence Audit

Report covering 'shadow flipping' rules for retirees, the impact of partial rental use on the Capital Gains exemption, and the 2026 'Empty Homes' tax pitfalls across Canada.

Calculate Your Potential Net Unlock

See how relocating or deferring property taxes changes your 30-year cash flow.

Launch Forensic Engine